Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

hello@myriadassociates.com

hello@myriadassociates.com

Museums & Galleries Exhibition Tax Relief :

Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

Museums & Galleries Exhibition Tax Relief :

Museums and Galleries Exhibition Tax Relief (MGETR) is a government funding incentive currently worth up to 36% of core production costs, with a higher rate of 40% for touring exhibitions. MEGTR is managed by HMRC and claimed as part of the Company Tax Return.

As your trusted MEGTR partner, Myriad will ensure your claim is accurate, compliant, and optimised.

Below are six simple sections to help you understand what Museums and Galleries Exhibition Tax Relief (MGETR) is, how it works and whether you’re eligible.

Museums and Galleries Exhibition Tax Relief (MGETR) is a creative industry tax relief incentive funded by the UK government.

Unlike other creative tax reliefs, there is no requirement for certification via a cultural test. MGETR supports museums and galleries to develop new permanent and temporary exhibitions for the benefit of the general public.

Museums and Galleries Exhibition Tax Relief is currently worth up to 36% of core production costs, with a higher rate of 40% for touring exhibitions.

Museums and Galleries can claim MGETR on the whichever is the lower:

The maximum repayable credit is capped at £100,000 for touring exhibitions and £80,000 for non-touring exhibitions.

To qualify for Museum and Galleries Exhibition Tax Relief, you need to meet the following criteria;

A touring exhibition has to fulfil the following additional criteria to qualify for Museums and Galleries Exhibition Tax Relief;

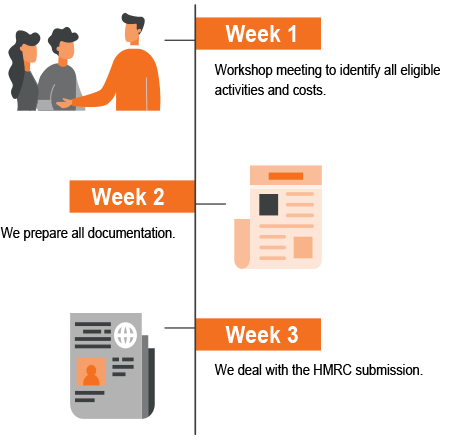

Museums and Galleries Exhibition Tax Relief is claimed as part of the Company Tax Return (CT600) filed with HMRC. You must also have the following information:

You’ll need to calculate if your exhibition has made a profit or a loss and determine whether your MGETR claim should be surrendered as a loss for a cash repayment or used to reduce your tax bill.

HMRC has a specific approach for calculating the taxable profit and loss of a Museums and Galleries Exhibition Production Company (MGEPC).

Qualifying costs are referred to as core expenditures. This general includes the spending on;

Non-core expenditure typically relates to the running and promotional costs for the exhibition; this includes;

To qualify for Museums and Galleries Exhibition Tax Relief you must be:

The Primary Production Company (PPC) is responsible for organising an exhibition at the first (if touring) or only venue (if not touring). It must also be responsible for the following at the first or only venue:

A Secondary Production Company (SPC) is responsible for organising an exhibition at the second or subsequent venues for a touring exhibition. It must be responsible for the following at its venue:

There is a cap on the amount of relief available via Museums and Galleries Exhibition Tax Relief.

The maximum repayable credit is capped at £100,000 for touring exhibitions and £80,000 for non-touring exhibitions.

An exhibition is a curated display of an organised collection of works, a single object or work considered to be of scientific, artistic, historical or cultural interest. The exhibition must be open to the general public irrespective of admission charge.

The following criteria would disqualify an exhibition from being eligible for Museums and Galleries Exhibition Tax Relief;

The apportionment method is not fixed and can be determined on a case-by-case basis. The key criterion is that it must be done fairly and reasonably.

There will often be more than one ‘fair and reasonable’ basis. The requirement is not that the apportionment must be made using the fairest and most reasonable basis but simply that it must be made on a fair and reasonable basis.

Step 1 of #

Is your business registered for Corporation Tax in the UK or are you a partnership with corporate owners?

Have you developed new or improved existing products, processes or services in the last 2 accounting periods?

Does your business have fewer than 500 staff, and either: A turnover of no more than €100 million; or Gross assets of no more than €86 million?

Sorry, you must be a UK limited company or be a Partnership with corporate owners to be eligible for R&D tax credits.

In order to qualify for R&D tax credits you must be seeking to advance science or technology within your industry. As you’ve not developed any new or improved any existing innovative tools, products or services, and not re-developed any existing products, processes or services in the last 2 years. It is unlikely you have any qualifying activity. If you’re unsure, email or call us and we’ll help clarify.

In order to claim R&D tax credits, you need to either employ staff or spend money on contractors, consumable items and other items. If you’re unsure, email or call us and we’ll help clarify.

Thanks for that!

Congrats!! Based on your previous answers, you will qualify for the SME scheme. If you’d like some help maximising and securing your claim, please email or call us.

Congrats!! Based on your previous answers, you will qualify for the RDEC scheme. If you’d like some help maximising and securing your claim, please email or call us.

Speak to an expert Back